Practical Implications of Anti-Dilution Protection

Getting real

In recent articles we’ve looked at anti-dilution protection. Recapping:

· An investor in any given round of financing is concerned that the next round could be at a lower price per share than what he is paying this round.

· The investor will insist upon anti-dilution protection.

·

There are two common types of anti-dilution protection:

full ratchet and weighted average.

We’ve covered the mechanics of anti-dilution protection. Now let’s look at what it really means.

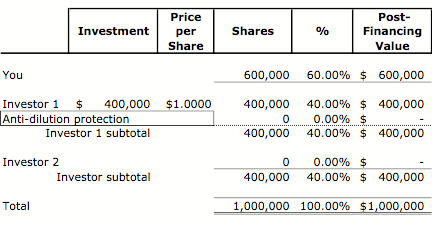

The Starting Position

First we will review

the example transactions. I agreed to invest $400,000 for 40% of your company’s

equity. The results of this investment are shown in the following table.

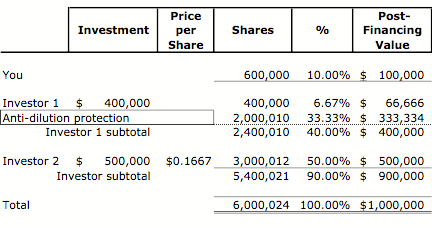

The Down Round

It’s time to raise some more money. Unfortunately, the only investment offer you are able to attract is at a lower valuation than the prior round.

· The new investor offers to invest $500,000 for 50% of your company.

· If 50% of the company is worth $500,000, then the pre-financing value of the company is $500,000.

· The $500,000 of pre-financing value is divided among you, my anti-dilution protection, and me.

Let’s look at how this would play out with the two different types of protection.

Full Ratchet Anti-Dilution Protection

As a practical matter, full ratchet anti-dilution protection gives the original investor rights to that number of shares of common stock as if I paid the current round’s lower price. The share price must meet the conditions that the new investor gets 50% of the equity and I get my full ratchet anti-dilution protection. Instead of $0.50 per share as might be inferred from the investment offer, the actual share price is $0.1667.

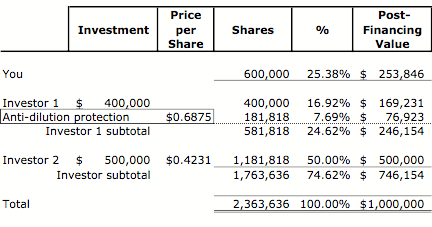

Weighted Average Anti-Dilution

Protection

Weighted average anti-dilution protection gives consideration to the relationship between the total shares outstanding as compared to the shares held by the original investor. The formula is CP2 = CP1 * (A+B) / (A+C). These variables were defined in the prior article.

What Causes a Down Round?

Very simply, a down round happens when you accept an investment at a price per share lower than that paid in a prior round. Notice that the emphasis is on “you accept…” Anyone can offer anything. It only matters if you accept the offer.

Why would you accept such a deal? Most likely because you need the money and you don’t have any alternatives. How could you find yourself in this position? Some possible reasons include:

· You didn’t make your sales plan

· You didn’t complete your product

· Your current investors can’t invest any more money in your company

· Your current investors could invest more money in your company, but won’t

· Potential investors just don’t “get it”

· You’ve got too many people

· You’ve got too few people

· You have the right number of people, but they aren’t the “right” people

· Your business model is flawed

· You don’t have a business model

· Private equity markets suck and you’re lucky to get any offer

The fact of the matter is that it doesn’t really matter why the down round happens.

Participants in the Investment

Let’s look at the participants in the investment, and their relative positions:

·

You – You still believe in your dream. You are still convinced that you’ve got

a great business opportunity.

Sure, you haven’t hit plan, but what entrepreneur does? You are willing

to accept a down round if it gives you another time at bat, and

you’ve got enough equity in your company to make it worthwhile.

· Me (the current investor) – Even if you (and your company) have done everything that you “should” have (exceeded plan, built out the management team…), I’m aware that I am vulnerable if only one next-round investor is at the table.

Knowing this, the primary way to avoid a down round is for the current investor(s) to do an “inside round,” in which the investors (at least the major investors, and quite possibly all investors) in previous rounds take their pro rata shares of an alternative round of financing. As mentioned in previous articles, such inside rounds are usually structured as an extension of the most recent round, or as a convertible note.

If I don’t step up, I am pretty much at the mercy of the new investor. Yes, I’ve got all sorts of legal protections built into my deal, including anti-dilution protection, but how meaningful are they really?

· The New Investor – He wouldn’t be looking at the deal unless he thought the fundamental business was promising and that he could achieve a superior rate of return. Of course that rate of return will be greatly impacted by the valuation of the company at the time of his initial investment. Obviously, the lower that value, the better for the new investor. But no matter how low the valuation, if the business doesn’t have that promise, there’s no deal to be done at any price.

OK, so how does the new investor view the other participants?

As far as the new investor is concerned, I don’t have much to offer. Unless I have agreed to invest a significant amount in the new investor’s round, he doesn’t have any incentive to care about me.

You, though, are the jockey he’s betting on. The new investor has been able to understand how the company has gotten to this point, is willing to “give you the benefit of the doubt,” and is willing to back you. You are important to him.

With

these dynamics in place, the new investor will want to keep you relatively

happy (under the circumstances) and is likely to dictate terms to me, insisting

that I waive or significantly modify my rights and protective provisions.

If

only one investor is interested in doing the next round, the Golden Rule

prevails – “He who has the gold rules!”

Anti-dilution protection will receive particular attention.

o Note that in the case of full ratchet anti-dilution protection, your share of your company will drop from 60% to 10%! This will not be acceptable to the new investor. He wants you to be satisfied by the terms of the deal, and he doesn’t really care about me. The new investor will demand that I waive my full ratchet anti-dilution protection.

This is likely to be presented as “take it, or leave it.” If I don’t agree, the new investor is likely to threaten to walk away from the deal. This is a game of Chicken that I’m not likely to win.

o With weighted average anti-dilution protection, your share of the company is reduced from 60% to 28%, almost all of which is caused by the valuation decline and not my anti-dilution protection. This level of protection is much more likely to be honored.

The bottom line is that under most circumstances full ratchet anti-dilution protection will be completely waived, while weighted average is likely to be accepted.

Frank Demmler

is Associate Teaching Professor of Entrepreneurship at the Donald H. Jones

Center for Entrepreneurship at the Tepper School of Business at Carnegie Mellon

University. Previously he was president & CEO of the Future Fund, general

partner of the Pittsburgh Seed Fund, co-founder & investment advisor to the

Western Pennsylvania Adventure Capital Fund, as well as vice president, venture

development, for The Enterprise Corporation of Pittsburgh. An archive of this

series of articles can be found at my

website.