Full Ratchet Anti-Dilution Protection

In last week’s article, we discussed how the word “dilution” has several meanings in deal making. It is critical to understand the context.

If pressed for justification, the investor may explain that if the value of a company declines between rounds, management must be largely responsible. The investor maintains that he shouldn’t be penalized for management’s deficiencies.

There are two common types of anti-dilution protection:

full ratchet and weighted average.

This week we will examine full ratchet anti-dilution protection.

Full Ratchet Anti-Dilution Protection

As a practical matter [as compared to the legal language below], full ratchet anti-dilution protection gives the original investor rights to that number of shares of common stock as if he paid the current round’s lower price.

I’ve tried to keep unnecessary complexity out of these articles, but it’s unavoidable at juncture.

Investors purchase preferred stock that is convertible into common stock. Initially the conversion is on a one-to-one basis, or at the same share price as that paid for the preferred stock. Anti-dilution protection is implemented by adjusting the conversion price.

The language that is used in a term sheet to say this is:

In the event that the Company issues additional

securities in the future at a purchase price less than the current Series A

Preferred conversion price, such conversion price shall be adjusted in

accordance with the following formula:

Full-ratchet – the conversion price will be reduced

to the price at which the new shares are issued.

National Venture Capital Association

Let’s look at how this works.

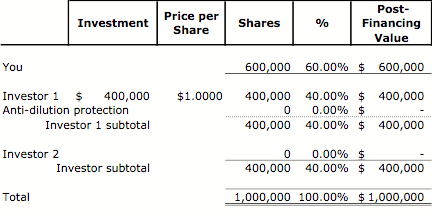

The First Round

Let’s review last week’s example.

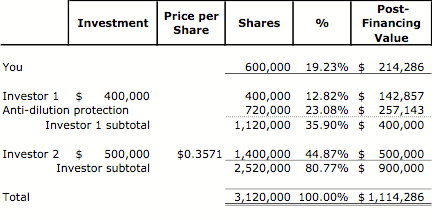

· I offer to invest $400,000 in your company in exchange for 40% of it.

· Since you own all 600,000 shares of your company, I am offering to buy 400,000 new shares in order to acquire 40%.

· My investment of $400,000 divided by 400,000 shares that I’m buying yields a per share price of $1.00.

· Since you own 600,000 shares, that means the value of the stake in your company is $600,000, which is the pre-financing value.

· Adding my $400,000 to that yields a post-financing value of $1,000,000.

· That is confirmed by taking the total number of outstanding shares, 1,000,000 (your 600,000 and my 400,000) and multiplying that by the share price of $1.00.

· That also says that the post-financing value of your company is $1,000,000.

There’s one big difference this week. The terms of this

deal include full ratchet anti-dilution protection.

The Second Round

It’s time to raise some more money. Unfortunately, the only investment offer you are able to attract is at a lower price per share than the prior round.

Without anti-dilution protection, the deal would proceed:

· The new investor offers to invest $500,000 for 50% of your company.

· If 50% of the company is worth $500,000, then the total company must be worth $1,000,000.

· Since there are 1,000,000 shares outstanding today and they will represent 50% of the company after the financing, then the new investor is buying 1,000,000 shares.

· The $500,000 investment divided by 1,000,000 shares yields a share price of $0.50.

· Since I paid $1.00 per share, I’m not happy. In fact, the 400,000 shares that I paid $400,000 for are now worth $200,000 (400,000 shares X $0.50 per share).

· The value of my investment has been diluted.

· In addition, the percent of the company I own has decreased (been diluted) from 40% to 20%.

· By the same reasoning, your equity stake is now only worth $300,000, and you’ve only got $500,000 of investor’s money to keep your business alive.

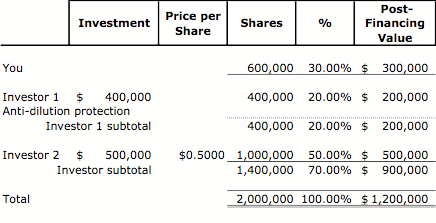

BUT I do have anti-dilution protection, so the deal will have needs to be adjusted.

The Adjustment – Step #1

With anti-dilution protection, the deal would proceed:

·

The new investor offers to invest $500,000 for 50%

of your company.

· If 50% of the company is worth $500,000, then the total company must be worth $1,000,000.

· Since there are 1,000,000 shares outstanding today and they will represent 50% of the company after the financing, then the new investor is buying 1,000,000 shares.

·

The $500,000 investment divided by 1,000,000 shares

yields a share price of $0.50.

· While I paid $1.00 per share, the new round will reduce that price to $0.50. So, in addition to the original 400,000 shares for which I paid $400,000, I will receive an additional 400,000 shares, bringing my total shares to 800,000 ($400,000 divided by $0.50 per share).

Done? Nope.

By issuing an additional 400,000 shares, the total number of shares has increased as well. The new investor would only own 42% if we were to stop here, but we won’t.

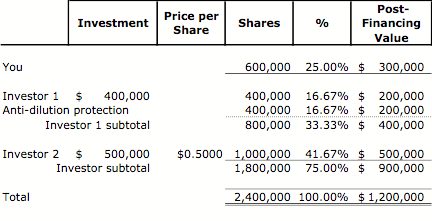

The Adjustment – Step #2

Remember the first element of the deal:

·

The new investor offers to invest $500,000 for 50%

of your company.

· If 50% of the company is worth $500,000, then the total company must be worth $1,000,000.

· Since there are 1,400,000 shares outstanding, including those created by my anti-dilution protection, the new investor must buy 1,400,000 shares to purchase 50%.

· The $500,000 investment divided by 1,400,000 shares yields a share price of $0.36.

Done? Nope.

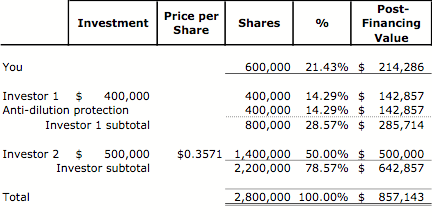

The Adjustment – Step #3

With the share price having dropped to $0.36, my anti-dilution protection needs to be recalculated

· Since the price per share this round is $0.36, in addition to the original 400,000 shares for which I paid $400,000, I will receive an additional 720,000 shares, bringing my total shares to 1,120,000 ($400,000 divided by $0.36 per share).

Done? Nope. Beginning to see a pattern?

The Adjustment – Steps #4-?

When I get additional shares from anti-dilution protection,

the investor’s ownership drops to less than 50%.

The share price is reduced so that the investor is buying

enough shares to own 50%.

The lower price means I get more shares. That lowers the

investor’s share price. And on and on…

This why I learned to use the “Iterate” function in my

spreadsheet.

The Investor Outcome

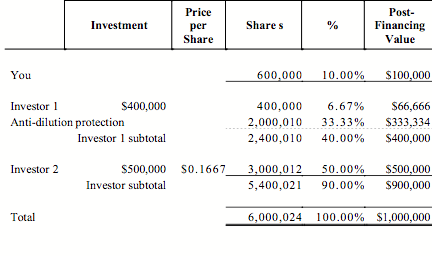

The share price drops all the way to less than $0.17.

The new investor buys 3,000,012 shares.

I get 2,000,010 shares as a result of full ratchet anti-dilution protection.

Your Outcome

As you may have noticed, all of these adjustments have occurred to the investors’ positions. What happens to you?

It isn’t pretty. As the number of shares for the investors ratchet higher and higher, your number of shares remains constant at 600,000.

Your share of your company has fallen to 10%!

The value of your shares has dropped to $100,000!

Reviewing the Basics

Let’s look at some of the relevant basics.

· Deals are negotiated with percentages, but are structured with shares.

· The value of a company is determined by multiplying the total number of common shares by the most recent share price.

· Price per share = Amount of investment divided by the number of shares purchased.

As I’ve said before, these may appear to be pretty dry and boring gobblygook, but as we’ve seen, they can have very significant consequences.

Recap

Full ratchet anti-dilution protection is very friendly to the investor and is very harsh to the founder.

Next week we’ll look at weighted-average anti-dilution protection.

Frank Demmler

is Associate Teaching Professor of Entrepreneurship at the Donald H. Jones

Center for Entrepreneurship at the Tepper School of Business at Carnegie Mellon

University. Previously he was president & CEO of the Future Fund, general

partner of the Pittsburgh Seed Fund, co-founder & investment advisor to the

Western Pennsylvania Adventure Capital Fund, as well as vice president, venture

development, for The Enterprise Corporation of Pittsburgh. An archive of this

series of articles can be found at my

website.