What is your company worth?

(Fourth

in a series)

The response to this question is: Who’s asking? Why?

If you’re talking to a bank and looking for a loan, your company is worth its book value with some adjustments. If you’re trying to impress your neighbors, it’s whatever you want it to be. The truth is that closely held private companies don’t have a specific value.

The only time that it has a verifiable, specific value is at the time of an equity transaction. At the moment of the closing of that transaction a specific amount of money is being exchanged for a certain amount and type of equity. A valuation can be calculated. At all other times, any valuation you might use will have a very high degree of subjectivity attached to it.

Of all the issues that arise between investors and entrepreneurs, valuation is probably the one that first-time entrepreneurs are most concerned about. On a scale of 0 to 10, they give valuation an importance level, relative to all other elements of a deal, an 8 or 9. They seem to think that there is a single valuation that is correct and that this number is the result of objective analysis and calculation. Wrong!

First, valuation is a very complex issue and cannot be judged without taking the other features of the proposed transaction into consideration. We will probe those other features in future columns. But to give you some sense as to their importance in my opinion, on that scale of 0 to 10, I would probably put valuation at a 5 or less.

OK, back to valuation.

The textbook approach that many entrepreneurs are taught goes as follows:

· Take the fifth year financial projections from your business plan (you do have a plan, don’t you?).

· Determine a price/earnings ratio (P/E) for public companies in your industry, and adjust it for what you think it will be in five years.

· Apply that P/E to your fifth year earnings. That is the potential value of your company in five years, assuming it could go public.

· Discount that number by the Internal Rate of Return (IRR) that potential investors in your company will be seeking (40% would be a good guess). That gives you the theoretical value of your company today.

· Divide the amount of investment by that valuation, and that will be the percent of your company that you will be willing to sell to the investor.

Seems reasonable. Probably is in many respects. But it has little-to-no-bearing on the valuation you will discuss with an investor.

What is your company worth? It’s worth whatever someone is willing to pay for it. If that someone is a professional investor, he will be willing to pay some value that is comparable to what other relevant companies have received in relatively recent transactions. In addition, any given investor will also adjust that value to be consistent with other deals that investor has done.

By now, you’re probably impatiently thinking, “All right. All right. But what’s the answer? What’s my company worth?”

Here’s my answer. Your company is worth some value within a range. Let me explain.

As you’ve gathered by now, determining valuation is a largely subjective process. Certainly, crunching numbers on spreadsheets, doing sensitivity analyses, and other quantitative methods are used to calculate different values under different sets of assumptions, but the actual value that an investor will propose is based upon his experience. Valuation is more an art than a science.

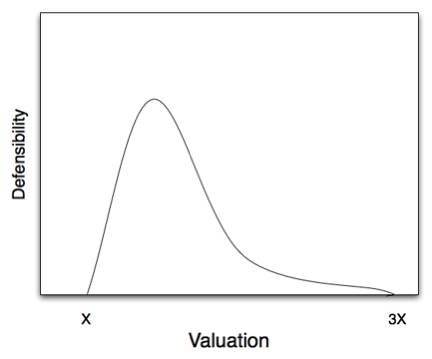

In the context of raising money, there’s some number below which an entrepreneur would not be willing to accept an investment. Similarly, there’s some number above which an investor will walk away. Voila: we’ve got a range! While not a science, a reasonable estimate of the range is between X and 3X, where X is the minimum value you (the entrepreneur) are willing to consider. In today’s fund raising environment, the value of X for a seed investment is likely to be in the range of $500,000 to $1,000,000.

See how the curve peaks on the left and trails off to the right? The left scale represents the reasonableness or defensibility of the valuation. The lower the value, the more likely that a reasonable set of variables can be used to justify the value. The higher the value, the greater the risk.

Since investors want to lower risk and maximize the return on investment, the valuation they are likely to propose will be toward the low end of the range. We’ll save a discussion of what the entrepreneur can do to try to get higher in the range for a future column.

Advice to entrepreneurs

You need to begin preparing for these discussions TODAY.

1. Build a network of mentors and advisors who are active in the deal network. They will have awareness of recent transactions and valuations.

2. Build a network of mentors and advisors of entrepreneurs who have “been there and done that,” particularly in your market space. They already have the battle scars. They know how valuations have evolved for their company. They can introduce you to other entrepreneurs in their network. They can introduce you to their investors.

3. Do your homework. Subscribe to the newsletters provided by such services as VentureReporter (venturereporter.net), and Venture Wire (www.venturewire.com), among others. Keep a log of relevant transactions.

As a first-time entrepreneur, you do not need to put yourself at the mercy of the investment community, but it’s your job, not theirs, to prepare yourself to engage in valuation discussions when you are seeking capital.

Frank Demmler (fd0n@andrew.cmu.edu) is Adjunct Teaching Professor of Entrepreneurship at the Donald H. Jones Center for Entrepreneurship at Carnegie Mellon University. (http://web.gsia.cmu.edu/display_faculty.aspx?id=168)